Key Takeaways

Shame-Free Evaluation: Recognising that mistaking a want for a need is a universal human vulnerability, not a personal financial failure.

The Power of Hindsight: True financial discipline isn't born at the cash register; it is forged during post-purchase reconciliation when the dopamine clearout occurs.

The Value-Time Scale: Implementing an escalating waiting period relative to an item's price tags shifts purchases from emotional impulses to intentional choices.

Fluid Categorisation: Understanding that certain "wants" genuinely transition into psychological or functional "needs" when they verifiably protect health or family dynamics.

The Blurred Lines of Modern Spending

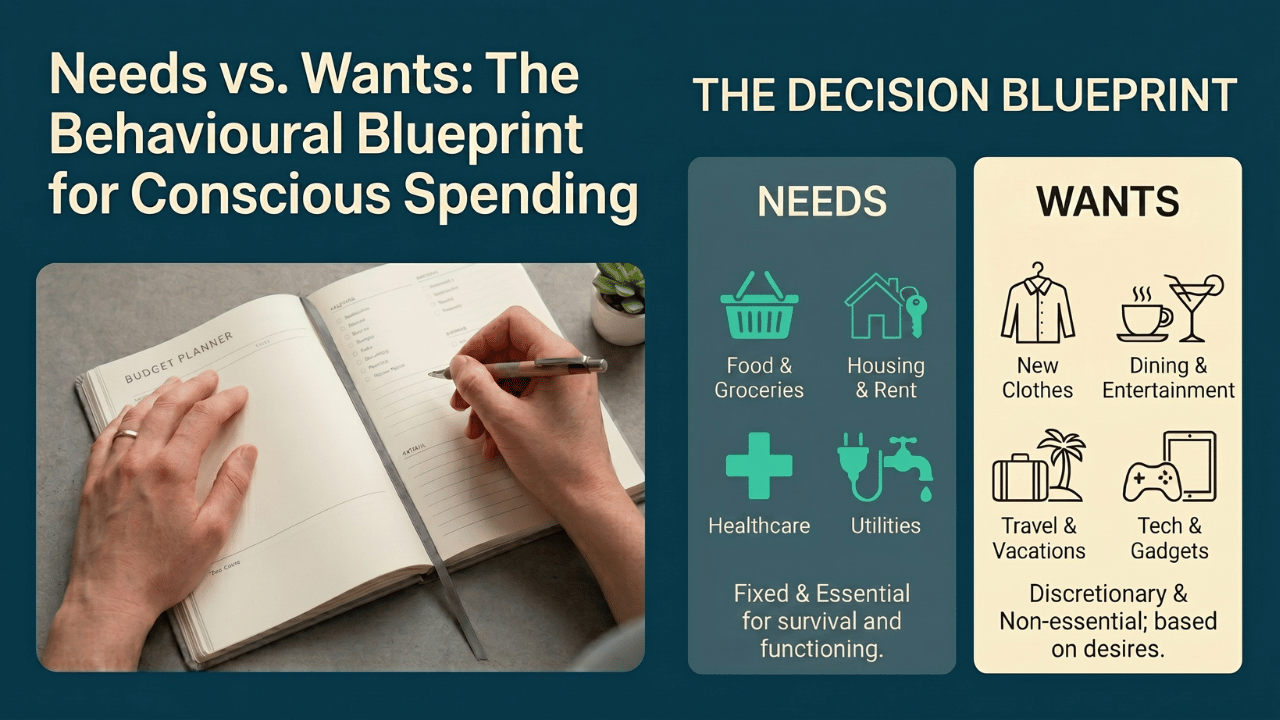

The standard financial advice dispensed across books and blogs makes an incredibly flawed assumption: it assumes that human beings are perfectly rational computing machines. We are told that distinguishing a need from a want is simple. A need keeps you alive; a want keeps you entertained. Food is a need; a restaurant dinner is a want. Water is a need; a sparkling water is a want.

Yet, anyone who has ever stood in a grocery aisle at 9 PM after a brutal 14-hour workday knows that these clean, academic boundaries shatter instantly under stress. You grab that luxury bar of chocolate or that premium coffee pod, and in that exact moment of exhaustion, your brain convinces you it is an absolute necessity for your survival.

This is the psychological mirage of modern consumerism. We use consumption as an emotional shock absorber. When we look at our bank accounts at the end of the month, we are often met with a staggering realisation: a significant portion of our capital has vanished into a black hole of micro-transactions that we labeled "essential" in the heat of the moment, but recognise as completely frivolous in the cold light of day.

For the vast majority of us, a financial tracking tool isn't a shield used at the point of sale to block every bad decision; it is a diagnostic tool used after the fact. We swipe the card first, and then we reconcile our accounts later. This creates an inevitable gap between the moment of impulse and the moment of realisation.

If we treat this gap as an opportunity for self-flagellation, our budget fails. If we treat it as data for future course correction, our wealth grows. Building sustainable spending habits isn't about achieving a state of robotic perfection where you never buy a comfort item again. It is about building a system of conscious awareness that allows you to glance backward at your choices, extend yourself a degree of psychological grace, and use that insight to cultivate authentic discipline moving forward.

Redefining the Foundations Without the Guilt

The True Anatomy of a Need vs. a Want

To fix a broken relationship with money, we must first establish clear, workable definitions that factor in human nature. In traditional economics, a Need is defined strictly as an expenditure required to maintain basic survival, health, and employment. This includes baseline groceries, basic shelter, primary healthcare, utilities, and the minimum transportation required to get to work. A Want, by contrast, is defined as any expenditure that enhances your lifestyle but is non-essential to your basic survival or livelihood.

However, when you are actively trying to improve your spending habits, these stark definitions can feel incredibly restrictive, leading to an immediate sense of deprivation. The moment a budget feels like a prison sentence, the human mind rebels, triggering a cycle of binge-spending.

To break this cycle, we have to look at these categories through a more fluid lens. A need is something that, if removed entirely, would cause immediate, tangible harm to your life or livelihood. A want is something that, if removed, would merely cause a temporary wave of psychological discomfort or boredom.

The Post-Purchase Mirage: Why We Justify Wants as Survival Tools

The human brain possesses an extraordinary capacity for narrative justification. When we want something intensely, our internal monologue goes to work to reclassify that item as a structural necessity. We don't just want the upgraded smartphone; we tell ourselves we need it because our current device's battery might degrade during an emergency. We don't just want the convenient takeout meal; we tell ourselves we need it because cooking dinner will cost us valuable professional productivity time.

This cognitive distortion occurs because our brains hate experiencing cognitive dissonance - the uncomfortable state of holding two conflicting beliefs, such as "I am trying to save money" and "I am about to spend money on something I don't need." To resolve this tension, we simply change the label of the purchase.

The danger here isn't the purchase itself; it is the self-deception. When we mislabel a want as a need, we rob ourselves of the opportunity to make a conscious choice. We act as if our hands were forced by external circumstances, which completely strips away our financial agency.

Overcoming this requires a willingness to catch yourself in the act of justification. It means standing at the counter and saying: "I am choosing to buy this luxury item because it brings me comfort right now, and that is okay - but it is a want, not a need." This simple shift in language preserves your control over your finances.

| Aspect | The Traditional Binary Framework | The PocFin Fluid Framework |

| Primary Philosophy | Strict, unyielding rules based on physical survival. | Adaptive, awareness-based logic that accounts for emotional realities. |

| Core Goal | Eliminate all non-essential spending through restriction. | Optimize spending by aligning money with conscious priorities. |

| Emotional Response | Triggers guilt and shame when a boundary is crossed. | Encourages self-correction and strategic adaptation. |

| Tracking Timing | Assumes real-time denial at the checkout counter. | Leverages deliberate post-purchase evaluation to build habits. |

Introduction to the Envelope Method: Digitizing Physical Discipline

For generations, the most reliable mechanism for enforcing this level of clarity was the physical envelope budgeting method. Individuals would withdraw their entire monthly income in physical cash and divide it across labeled paper envelopes: Rent, Groceries, Fuel, and Entertainment. If the Entertainment envelope ran completely dry on the second week of the month, the spending stopped dead. There was no digital abstraction, no overdraft protection, and no psychological trickery; the physical absence of cash served as an absolute boundary.

In an increasingly cashless economy dominated by tap payments, digital wallets, and instant credit lines, this tactile friction has been entirely erased. Spending money has become completely effortless, while tracking where it went requires conscious, deliberate energy. To combat this digital drift, we must actively port the core mechanics of the envelope system into our daily digital routines.

Don't treat your digital tracking tool as a passive archive or an automated dashboard that simply categorises your past mistakes for you without your input. Treat it as your digital envelope stack. When you sit down to manually input and reconcile your bank transactions against your budget categories, you are recreating the precise tactile friction of the physical envelope method. This manual entry forces an intentional pause, turning an automated bank alert into a moment of active, conscious self-evaluation.

By translating the physical boundaries of cash into an intentional digital habit, you introduce a vital layer of structural resistance back into your financial ecosystem. This structure is precisely what bridges the gap for individuals who find themselves consistently struggling to maintain baseline control over their monthly income.

For those looking to transition from basic tracking to building a comprehensive blueprint, integrating these structured buckets serves as the bedrock for long-term consistency. To explore the foundational mechanics of this approach in greater depth, reviewing a structured strategy like The Envelope Budgeting Method: From Physical Cash to Digital Discipline can offer a practical, step-by-step pathway forward.

The Forensic Audit of Your Transaction History

Facing the Mirror: The Emotional Weight of Looking at Past Spend

Moving from basic awareness to real behavioral change requires stepping into what is undeniably the most uncomfortable phase of financial development: the forensic audit. This is the process of opening up your transactional records from the past 30 to 90 days and looking directly at exactly where your currency flowed.

For someone trying to better their spending habits, this process is rarely just an administrative exercise; it carries an intense emotional weight. Reviewing an endless stream of uncoordinated retail purchases, half-utilised subscriptions, and impulsive weekend expenditures forces you to face internal patterns of weakness, stress, and lack of restraint.

Review Past Transactions ─> Encounter Behavioural Vulnerabilities ─> Experience Emotional Discomfort ─> Choice: Disengage OR Lean into Discipline

It is completely natural to feel an immediate urge to turn away, close the app, and promise to "do better next month" without actually analysing the data. This defence mechanism protects our self-image, but it leaves our destructive habits completely intact.

The breakthroughs happen when you realise that your past transaction history isn't a moral scorecard detailing your worth as a person; it is purely a historical data set detailing your past emotional states. Every single impulse buy was simply an attempt to solve a problem - usually boredom, exhaustion, or anxiety - using capital instead of internal coping mechanisms. By stripping the shame away from the data, you can look at your spending history with the objective curiosity of a scientist trying to understand an experiment, rather than a judge handing down a sentence.

The Hindsight Framework: Categorising Transactions After the Dopamine Fades

Because the majority of modern tracking happens after the card has cleared, our primary tool for behavioural correction is the Hindsight Framework. When you are standing in a store or browsing an online portal, your brain is flooded with dopamine - the neurotransmitter of anticipation. This chemical cocktail actively distorts your judgment, artificially inflating the utility of the item you want.

It is only hours or days later, once the item is sitting in your home and the chemical baseline returns to normal, that your perspective clears. This post-dopamine window is where real financial education takes place.

| Point of Sale | Post-Purchase Window |

| Brain flooded with Dopamine | Chemical baseline returns to normal |

| Artificially inflates utility | Perspective clears completely |

| Distorts long-term judgment | Accurate assessment of utility |

When you enter your transactions into your budget retroactively, ask yourself a simple diagnostic question for any non-essential item: "Knowing what I know now, if I could press a button and return this item for a full cash refund, would I do it?"

If the answer is an immediate yes, you have successfully isolated an emotional want that masqueraded as a need. By systematically running this diagnostic check during your weekly check-ins, you begin to build a mental library of your specific spending triggers. You start to see patterns: perhaps you consistently overspend on food delivery on Thursday nights, or you buy clothing items you never wear when you are feeling stressed on Sunday afternoons. This awareness is exactly what creates the critical mental space you need to step in and pause before you make your next purchase.

If you find that your overall system continually falls apart during this diagnostic phase, it is highly likely that your underlying categories are simply too rigid to survive real-world human behaviour. To correct this, shifting toward a highly adaptable framework can provide the necessary structural flexibility. Learning How to Create a Budget You’ll Actually Stick To can give you the precise operational tools required to transform these painful historical insights into a sustainable, resilient monthly budget.

Navigating the Grey Areas: When a "Want" Serves a Deeper Purpose

The traditional narrative of personal finance treats any expenditure outside of strict survival as a net negative - a leak in your financial bucket that must be plugged with raw discipline. But life is not a spreadsheet, and human beings are not linear programs. If you classify every single comfort, hobby, or lifestyle upgrade as an unacceptable indulgence, your financial system will eventually crack under the pressure of psychological fatigue.

The breakthrough in intermediate financial discipline is recognising the existence of the "Grey Area." A Grey Area purchase is an expenditure that is technically classified as a want under strict economic definitions, but practically serves a vital, functional role in protecting your physical health, mental well-being, or family cohesion.

Consider a high-quality mattress, a gym membership, or a reliable piece of software that streamlines a chaotic workflow. If you look at these purely through the lens of baseline physical survival, they are non-essential. You can sleep on a cheap mattress, exercise for free on the pavement, and manage your life with a tangled web of manual spreadsheets.

However, when you analyse the downstream impact of these choices, the math shifts:

| The Cheap Choice | The Real Downstream Cost |

| Lumpy, cheap mattress | Bad sleep, back pain, and feeling exhausted at work. |

| No structured fitness plan | Skipping workouts entirely, leading to higher medical bills later. |

| Messy, frustrating spreadsheets | Giving up on tracking entirely because it's too much of a headache. |

In these instances above, a strategic want behaves exactly like a preventive need. It serves as an investment in your personal infrastructure. The critical distinction between a healthy Grey Area purchase and a standard impulse buy lies in its long-term utility. An impulse buy provides a sharp spike of dopamine at the moment of acquisition, followed by an immediate slide into irrelevance or guilt. A valid Grey Area purchase provides sustained utility over an extended timeline, actively reducing friction in your daily existence and protecting your core assets: your time, your health, and your relationships.

When you’re logging your expenses in PocFin, don't feel guilty about these middle-ground purchases. Create a specific category for things like "Well-being" or "Life Upgrades." This keeps your spending honest without making you feel like you messed up your budget.

The Strategic Pause & Thinking Long-Term

The Proportional Wait Rule: Give Yourself Time to Think

When you start getting better at managing your money, the goal changes. You want to stop bad spending decisions before they happen. The easiest way to do this is to simply force yourself to wait.

Online shops are designed to make you spend money instantly. One-click checkouts, saved cards, and face scans are all built to let you buy things before your brain even has time to think about the consequences.

To beat this, you need to set up a simple rule: the more expensive the item, the longer you have to wait before buying it.

| Item Type | Price Range (ZAR) | How Long to Wait | The Goal |

| Small stuff (Takeout, random gadgets) | R50 - R500 | 24 Hours | Breaks the instant "I want it right now" urge. |

| Medium upgrades (Clothes, hobbies) | R501 - R5,000 | 7 Days | Shows if you actually need it during a normal week. |

| Big lifestyle purchases (Bikes, cars, tech) | R5,001+ | 14 to 30 Days | Lets the excitement wear off so you can see if it fits your life. |

Let's look at a real-world example: Staring at an online checkout cart for a custom bicycle for 14 straight days, watching the emotional impulse transform into a calculated lifestyle asset.

On day one, you're excited. You imagine yourself riding up mountains every weekend and completely changing your fitness routine. But by day ten, that initial excitement wears off. You start looking at the reality: Do I actually have the free time to ride this? Does our family budget comfortably absorb this?

If you still want it after two full weeks of thinking it over, you can buy it completely guilt-free. You know it’s a real choice, not just a passing whim.

The True Cost of a Purchase: Today's Luxury vs. Future Freedom

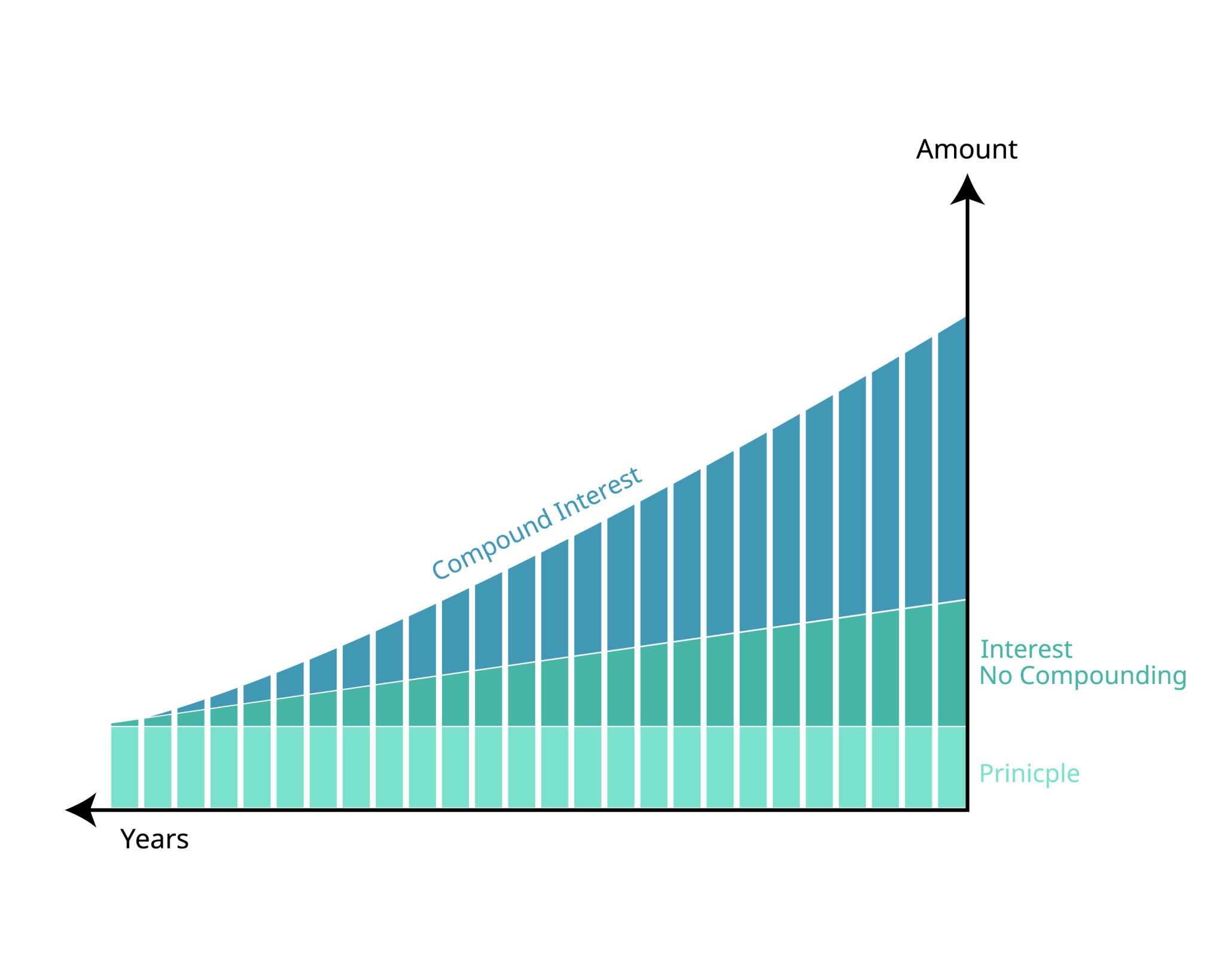

When you buy a want, you aren't just spending the cash in your hand right now. You are also giving up what that money could have earned if you invested it instead. This is called opportunity cost.

Let's look at the math without the confusing academic jargon. Imagine you decide to skip an unnecessary R3,000 monthly luxury and invest that money instead at a standard 10% annual growth rate.

Because of how interest builds on top of interest over time, that small monthly choice turns into massive numbers:

In 10 Years: Those R3,000 monthly decisions add up to R614,534.40.

In 20 Years: That same monthly habit turns into R2,278,105.20.

Suddenly, you aren't just choosing between a retail item and an empty bank account today. You are choosing between a temporary comfort right now and millions of rands of financial freedom later.

Automating Grace: Let Your Budget Roll with the Punches

A budget that is too strict will always break. If your entire plan falls apart because you spent a bit too much on a night out or bought something impulsive, you'll eventually get frustrated and quit. Real financial systems need to be flexible. We call this Automating Grace.

There will always be months where you spend more than you planned - like during the holidays or birthdays. Instead of seeing this as a failure, your budget should handle it automatically.

By letting your category balances roll over between months, you remove the stress. If you overspend by R1,500 in December, that negative balance simply moves into January, giving you R1,500 less to spend for that new month. Your long-term savings stay perfectly safe, and your budget naturally corrects itself without you needing to panic.

Use PocFin’s carry-over features to handle these moving categories. When you go over budget in a fun category, don't move money out of your savings to fix it. Let the negative balance roll over into next month. It gives you a natural reason to spend a bit less next month, keeping your big financial goals perfectly on track.

Conclusion: Turning Mistakes into Progress

Mastering the lines between needs and wants isn't about having perfect willpower. It's about building a simple, forgiving routine that works with real human behaviour.

By using your tracking app to look back at your purchases honestly, you can figure out what triggers your impulse spending without beating yourself up over it. Using simple tools like the waiting periods ensures you're making choices you won't regret later.

True financial freedom doesn't mean you have to stop enjoying your life. It just means that when you do spend money on a want, you do it with clear eyes and total control.

Actionable Next Steps

Look at the numbers: Go through your past 30 days of transactions and ask yourself if you'd take a cash refund on them right now if you could.

Find your triggers: Notice when you tend to spend impulsively (Are you tired? Stressed? Bored?).

Set a timer: Pick a waiting period for your next big purchase and stick to it.

Set up your carry-over: Make sure your variable categories are set to roll over so one bad month doesn't break your plan.

Cheers,

The PocFin Team