Before we dive into the mechanics of the market, here are the essential truths every investor needs to carry:

- Risk is the Price of Admission: You cannot achieve inflation-beating growth without accepting some level of price fluctuation.

- Time is the Ultimate Hedge: An 18-year-old can afford a market crash; a 64-year-old cannot. Your investment horizon dictates your risk capacity.

- Volatility ≠ Permanent Loss: Prices moving up and down (volatility) is normal; selling during a dip is what turns a temporary fluctuation into a permanent loss of capital.

- Diversification is Your Only Safety Net: Spreading your bets across different risk types is the only way to protect your wealth from the failure of a single company.

Why Risk Isn’t a Four-Letter Word

In the world of finance, "risk" is often treated like a looming shadow - something to be avoided at all costs. However, if you're looking to build long-term wealth, avoiding risk entirely is actually the most dangerous path you can take. Why? Because the safest place for your money - a standard savings account or under a mattress - is virtually guaranteed to lose purchasing power over time due to inflation.

Think of risk not as a danger, but as a variable. When you buy a stock, you are essentially making a trade: you give up the certainty of your cash today for the probability of more cash tomorrow. The type of stock you choose determines how much uncertainty you are willing to stomach in exchange for that potential growth. Whether you are an 18-year-old with forty years of earning power ahead of you or someone nearing the golden years of retirement,

understanding these layers of risk is the difference between a portfolio that thrives and one that withers. A Tale of Two Investors: Imagine an 18-year-old who watched their first investment drop 30% in a month; they stayed calm, knowing they had decades to recover. Contrast this with a retiree who saw the same drop and realised their grocery budget for the next five years just evaporated - the risk didn't change, but the consequences did.

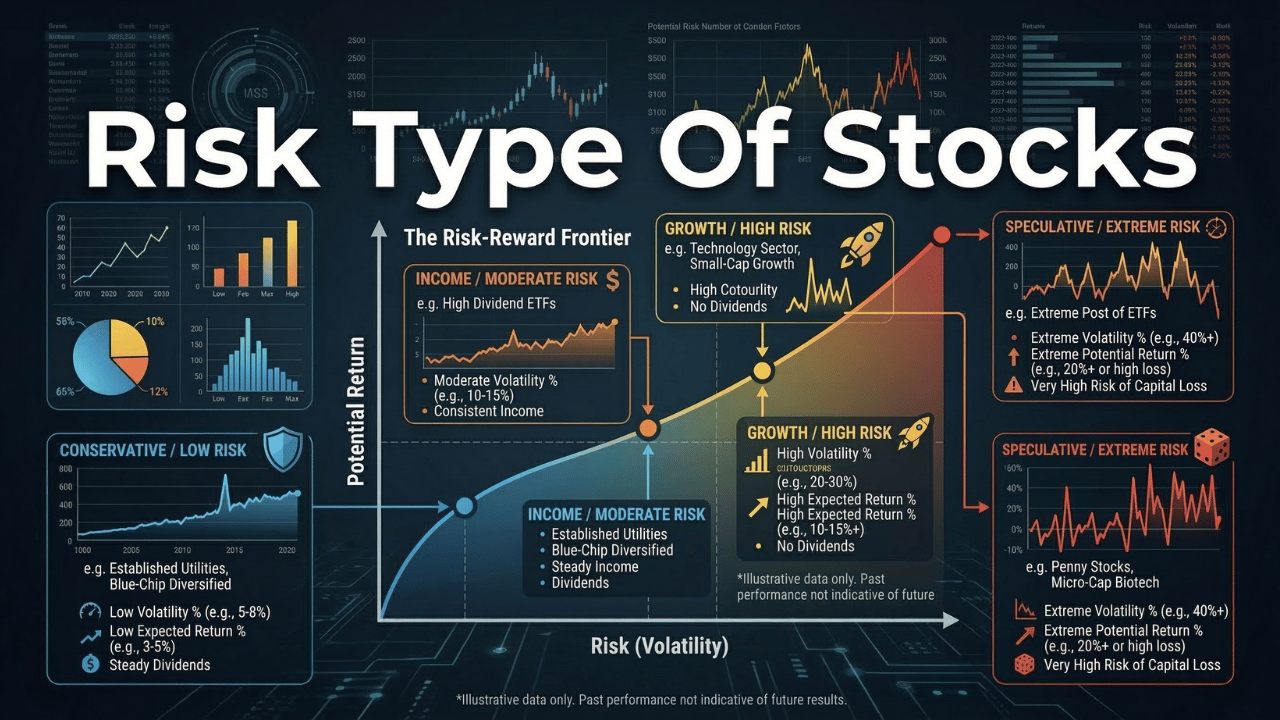

Level 1: The Foundation - Understanding the Risk-Return Spectrum

To navigate the stock market, you must first understand that not all risks are created equal. In academic finance, we split risk into two distinct buckets: Systematic and Unsystematic.

1. Systematic Risk (Market Risk) This is the big picture risk. It’s the risk that affects the entire market at once. Think of a global pandemic, a sudden hike in interest rates by the South African Reserve Bank, or a global recession. No matter how safe your individual stocks are, they will likely all feel the tug of a systematic downturn. You cannot diversify away from systematic risk; you can only decide how much of it you are willing to endure.

2. Unsystematic Risk (Specific Risk) This is the risk inherent to a specific company or industry. For example, if a CEO is caught in a scandal or a mining company strikes a poor-quality vein, that company's stock might plummet while the rest of the market stays flat. The good news? This risk can be mitigated. By owning 20 or 30 different stocks across different sectors, the failure of one won't ruin your entire portfolio.

The Inflation Risk: The Silent Wealth Killer

Many beginners believe that low risk means no loss. However, we must address the most subtle risk of all: Inflation Risk. If the cost of living in South Africa rises by 6% annually, but your safe investment only returns 4%, you are effectively becoming 2% poorer every year. To truly build wealth, your primary goal is to exceed the inflation rate significantly. This is why understanding What is Investing And How To Get Started Investing In South Africa is so critical - it’s about moving from saving to growing.

Level 2: Low-Risk Stocks - The Sleep-Well-at-Night Portfolio

If you are a conservative investor or someone nearing retirement, your focus shifts from aggressive growth to Capital Preservation and Income. Low-risk stocks are the bedrock of a stable portfolio. These companies are often referred to as Defensive because they defend your wealth during market downturns.

Defensive Stocks: The Essentials

Defensive stocks belong to industries that people cannot live without, regardless of the economy. Think of utilities (water and electricity), healthcare, and consumer staples (food, soap, and basic household goods). Whether the economy is booming or in a deep recession, people still need to eat, wash their clothes, and turn on the lights. Consequently, these stocks don't skyrocket during bull markets, but they also don't collapse when things get ugly.

Blue-Chip Titans

In South Africa, we look toward the JSE Top 40 for our Blue-Chips. These are massive, well-established companies with a long history of stable earnings. They are the titans of industry - think of the major banks or established retailers. Because these companies have huge cash reserves and dominant market shares, the risk of them going bankrupt is extremely low.

Income Stocks: The Power of Dividends

Low-risk stocks are often Income Stocks, meaning they pay out a portion of their profits to shareholders in the form of dividends. For a beginner, dividends are like a safety net. Even if the stock price stays flat for a year, you still receive a cash payout. When you combine these payouts with the concept of Compound Interest, you start to see how even "boring," low-risk stocks can create massive wealth over time. By reinvesting those dividends, you are buying more shares, which in turn pay more dividends - a cycle that creates an exponential growth curve.

Comparison: Blue-Chip vs. Defensive Stocks

| Feature | Blue-Chip Stocks | Defensive Stocks |

|---|---|---|

| Primary Goal | Stability & Moderate Growth | Capital Protection |

| Volatility | Low to Moderate | Very Low |

| Example Sectors | Finance, Telecoms, Tech Giants | Utilities, Healthcare, Food |

| Dividend Yield | Generally Consistent | High and Reliable |

While these stocks are low risk, don't mistake that for no risk. Always track the dividend payout ratio. If a company is paying out more than it earns just to keep shareholders happy, that safe dividend might be on the chopping block soon.

Level 3: Moderate-Risk Stocks - The Engines of Growth

This is where the majority of long-term investors spend their time. Moderate-risk stocks offer a balance: they have more "bounce" (volatility) than a utility company, but they offer much higher potential for capital appreciation.

Growth Stocks: Betting on the Future

Growth stocks are companies that are expected to grow at a rate significantly above the average for the market. These companies usually don't pay dividends; instead, they plow every cent of profit back into research, development, and expansion. When you buy a growth stock, you aren't looking for a check in the mail every quarter - you are betting that the share price will be significantly higher in 5 to 10 years.

Mid-Cap Gems: The Sweet Spot

Mid-cap stocks are companies that have moved past the risky startup phase but haven't yet become slow-moving giants. They have established business models but still have plenty of runway to grow. For many investors, this is the sweet spot of the risk-return spectrum - higher growth potential than blue-chips, but with more stability than small, unproven companies.

Cyclical Stocks: Riding the Economic Waves

Cyclical stocks are highly sensitive to the economy. In South Africa, our mining and manufacturing sectors are classic examples. When the global economy is booming, demand for resources like platinum, gold, and coal surges, and these stocks soar. When the economy slows down, they are often the first to drop. Investing here requires a bit more stomach for volatility and an understanding of market cycles.

Level 4: High-Risk Stocks - The Moonshots and Multi-Baggers

High-risk stocks are where fortunes are made—and where they can disappear in an afternoon. These investments are for the portion of your portfolio that you don’t need for rent or groceries. They are "aggressive" plays that benefit from a long time horizon or specialised knowledge.

1. Small-Cap and Penny Stocks

Small-cap stocks are companies with a smaller market valuation (often below R2 billion on the JSE). Because these companies are small, they can grow 10x or 100x more easily than a giant like Naspers. However, they are often "illiquid," meaning there aren't many buyers or sellers. If you need to sell quickly during a panic, you might find yourself stuck holding the bag while the price plummets.

2. Emerging Markets: Looking Beyond the Rand

While South Africa is an emerging market itself, high-risk investors often look toward "frontier" markets or volatile regions like parts of Southeast Asia or South America. These regions offer explosive growth as their middle class expands, but they come with massive political and currency risk. A sudden change in government policy can wipe out 50% of your investment's value overnight.

3. Speculative Tech and Biotech

In 2026, the high-risk spotlight is firmly on Artificial Intelligence (AI) and biotechnology. These companies often spend years in "burn mode," losing millions of rands while they develop a single drug or a new AI model. If they succeed, you win big. If their trial fails or their software is outcompeted, the stock often goes to zero. This is the definition of "all or nothing."

Growth vs. Value vs. Speculative (2026 Risk Profile)

| Feature | Growth Stocks | Value Stocks | Speculative Stocks |

|---|---|---|---|

| Risk Level | Moderate-High | Low-Moderate | Very High |

| Price/Earnings (P/E) | High (Paying for future) | Low (Undervalued) | N/A (Often no profit) |

| Time Horizon | 5–10 Years | 3–5 Years | 10+ Years (or Bust) |

| Volatility | High | Low | Extreme |

Level 5: Strategic Allocation - Matching Risk to Your Life Stage

The "best" stock isn't the one with the highest return; it’s the one that fits your current life stage.

The 18-Year-Old’s Edge

If you are 18, your greatest asset isn't money - it’s time. You can afford to put 80% or even 90% of your portfolio into high-risk growth stocks. If the market crashes tomorrow, you have 40 years of pay checks coming to wait for the recovery. In the long run, the bounce of the market is just noise on a chart that is trending upward.

A Tale of Two Eras: Imagine an 18-year-old in 2026 investing in a speculative green-hydrogen company. Even if the company fails, they’ve learned the mechanics of the market with a small amount of capital. If it succeeds, they’ve captured a "multi-bagger" that could fund a house deposit by the time they are 30.

The Mid-Career Pivot (Ages 35–50)

By now, you likely have more to lose. You have a family, a bond, and a retirement goal that is visible on the horizon. This is the stage for consolidation. You might shift to a 60/40 split: 60% in solid growth and blue-chip stocks, and 40% in more defensive income-generating assets. You are still growing, but you are no longer "gambling."

The Finish Line (Age 60+)

At this stage, you are shifting to Capital Protection. You don't have time to wait out a 5-year recession. Your portfolio should lean heavily toward defensive blue-chips and income stocks that provide the cash you need to live, without requiring you to sell your shares during a market dip.

Advanced Analysis: The Math of Risk

To graduate from a beginner to an advanced investor, you need to understand how professionals measure the bounce.

1. Beta: Measuring the Sympathy

Beta tells you how much a stock moves compared to the overall market (like the JSE Top 40).

- Beta of 1.0: The stock moves exactly with the market.

- Beta of 1.5: The stock is 50% more volatile. If the market goes up 10%, your stock goes up 15%. If the market drops 10%, your stock drops 15%.

- Beta of 0.5: The stock is half as volatile as the market. It’s a slow and steady performer.

2. Standard Deviation: The Consistency Gauge

While Beta compares a stock to the market, Standard Deviation measures how much a stock's price deviates from its own average. A high standard deviation means the price is all over the place (unpredictable). A low standard deviation means the returns are consistent and predictable.

Diversification: The Only Free Lunch

The only way to lower your risk without necessarily lowering your return is diversification. By owning stocks that are uncorrelated - meaning they don't all move for the same reasons - you smooth out the ride. If your tech stocks are down because of interest rates, perhaps your gold mining stocks are up as a safe haven.

Don't just diversify by company name; diversify by Risk Type. Owning ten different high-risk tech stocks isn't diversification - it’s a concentrated bet on tech. True safety comes from having a mix of Level 2, 3, and 4 stocks.

Building Your Personal Risk Roadmap

Investing is not a sprint; it’s a marathon where the terrain changes every few kilometers. There is no perfect stock, only the stock that is right for you right now.

If you are young, embrace the volatility. If you are established, protect your progress. But regardless of your age, the greatest risk you can take is staying on the sidelines while inflation erodes your future.

Next Step: Review your current holdings. Are you over-weighted in one risk category? Pick one sector you currently don't own - perhaps a defensive utility or a mid-cap growth gem - and research how it might balance your current bounce.

If the JSE dropped 20% tomorrow, would you be excited to buy the dip, or would you be unable to sleep? Your answer tells you more about your risk tolerance than any spreadsheet ever could.

Cheers,

The PocFin Team